“Strong rate activity” isn’t enough to turn around negative to low ROEs for US homeowners insurance carriers, the broker has warned.

More than half of US states under review produced negative Returns on Equity (ROE) for homeowners carriers, Aon has said.

With nearly all states producing a carrier ROE below the 10% cost of capital hurdle after investment gains, the broker said it was unlikely many insurers reported positive pre-tax income for underwriting US homeowners policies.

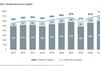

Aon launched its “Homeowners Return on Equity Outlook – October 2024” report, which analyses state and aggregate statutory filing data to estimate the prospective return on equity (ROE) for US homeowners business.

The report revealed prospective ROE for diversified homeowners insurance carriers had decreased by 100 basis points to just 5% from last year’s report, despite the significant rate increases that were achieved by carriers in 2023/2024.

The market’s dynamics highlight continued poor underwriting profit results over the past decade across the US homeowners line of business, resulting from increased insured losses, Aon reported.

These losses stem from a clutch of leading causes, according the broker: from secondary perils, such as severe convective storms (SCS); lower than previously expected lifespan of asphalt shingle roofs and their poor wind performance in windstorms including SCS events; and deductible increases not keeping pace with total insurable value (TIV) increases leading to greater net exposures for carriers.

The lack of consistent returns could deter the commitment of new capital to homeowners business, Aon warned.

Insurers should identify sources of capital, and quantify the appetite of that capital for various forms of risk, the intermediary suggested.

“In addition, there could be other creative approaches taken to roof coverage and loss sharing between the policyholder and insurer. Deductibles are another tool at the insurer’s disposal to address claim costs both for the roof as well as the entire structure and are a critical tool for combating the increase in insured losses,” Aon said.

“As further exposure growth enters high hazard areas, insurers should consider deterministic analyses to create a robust view of enterprise risk management, understanding location-level hazard and contribution to existing concentrations before binding a policy, evaluating a risk based on historical experience and catastrophe modelling and incorporating the full cost drivers into pricing,” the broker continued.

The Aon study suggested that, at prospective 2024 rates and before income taxes, homeowners insurers keep about one cent of profit for every premium dollar they earn. That direct profit must be shared between the primary carrier, reinsurance partners, and the US Treasury.

“Our data show that both policyholders and insurance carriers need to consider tools for loss mitigation and reduction for the line to find a long term profitable equilibrium,” said Paul Eaton, head of US actuarial of Aon’s strategy and technology group.

“Headline ROE numbers fail to illustrate the wide range of outcomes realized by insurers offering homeowners policies, and we expect insurers will earn meagre ROEs insufficient to support the underlying risk,” he said.

“In response to the challenges faced by U.S. homeowners insurers, Aon continues to provides strategic consulting services backed by Aon’s proprietary datasets, and implementation support, to effect change through an organization to align to business strategy,” Eaton added.

No comments yet